This simulator aims to answer a fundamental retirement question: given my current savings, spending plans, and market history, am I able to comfortably retire? Rather than making assumptions about the future, the tool replays your retirement scenario against every historical period in US market history — from the panic of 1907 to the dot-com crash to 2008 — and counts how often your plan would have survived.

The approach is known as historical backtesting. It does not predict what markets will do in your lifetime. What it does do is show you how your plan would have fared under all historical market conditions the US has ever experienced, giving you a realistic picture of the risk you are taking on. Obviously, if in the future we experience a larger stock market crash than ever seen before, this simulator will not predict it: it can only project based on what has happened previously.

This documentation explains every input field, every result tile, and the methodology behind the numbers. Because retirement planning decisions are consequential, we encourage you to read the Caveats & Limitations section before acting on these results.

The simulator uses the Shiller dataset, which records US stock market returns and inflation going back to 1871. This gives roughly 150 years of monthly data covering many complete market cycles: booms, crashes, recessions, high-inflation periods, and long periods of low growth.

All returns in the model are real (inflation-adjusted). When the simulator says your portfolio grew to $X, that $X has the same purchasing power as today's dollars. This means the simulation already accounts for inflation eroding your savings — you do not need to add an inflation adjustment separately.

The Shiller dataset also includes the CAPE ratio (Cyclically-Adjusted Price-to-Earnings ratio, also known as the Shiller PE). CAPE is used to assess current stock market valuations and adjust success rate estimates accordingly. CAPE is only used in one subsection of the results; the main part is not reliant on CAPE.

Each simulation run creates many independent "paths" — one for each possible historical starting month. There is more than 100 years of data, leading to more than 1200 simulated paths, each experiencing a different sequence of returns. The simulation then counts how many paths survived (did not go bankrupt before the retiree died) to compute a success rate.

For each path, the simulator runs a month-by-month loop:

- Add cash flows — any income (Social Security, pension) or expenses (mortgage, tuition) scheduled for this period are added to or subtracted from the portfolio.

- Update allocation — if you have set up a dynamic asset allocation strategy (a "bond tent"), the portfolio is rebalanced to the target allocation for this period.

- Withdraw — the planned withdrawal for living expenses is deducted. The chosen withdrawal method determines how much this is.

- Apply returns — the portfolio grows (or shrinks) according to the historical returns for this period.

- Check for bankruptcy — if the portfolio value falls below zero, the path is marked as bankrupt. If a reverse mortgage is available, it may rescue the path first.

The simulation uses standard actuarial mortality tables to model the probability of dying at each age. Rather than assuming everyone lives to a fixed age, each path is sampled against the mortality distribution: some paths end at 72, others at 89, others at 101. This creates a realistic spread of retirement durations.

Mortality matters because a retirement that "fails" at year 35 of retirement is not actually a failure if you are almost certain to have died by then. The success rate reported in the results already accounts for your actual probability of living that long. A retirement that only fails in scenarios where you would live past 100 has a much higher real-world success rate than the raw numbers might suggest.

Below is a detailed description of every input field in the simulator. Fields marked conditional only appear when certain other settings are active. Fields marked optional can be left blank.

This section establishes when you retire and what accumulation phase looks like before then.

- Retired / Retire Now — you are already retired, or retiring immediately. The simulation begins at step zero with your current portfolio.

- Specific Month or Year — you plan to retire at a particular date. The simulator adds your annual savings to the portfolio each period until that date. Your portfolio will also of course fluctuate up and down with the markets during this accumulation phase.

- Specific Portfolio Value — you plan to retire when your portfolio hits a target number. The simulator adds savings each period, in addition to regular market fluctuations, until the threshold is crossed.

Your current financial position — the starting point for the simulation.

If you would prefer not to rely on your home equity (perhaps because you intend to leave it to heirs, or would rather move to a rental at that point), leave this unchecked and a portfolio reaching zero will be counted as bankruptcy.

How you plan to draw money from your portfolio in retirement. Different strategies involve very different trade-offs between predictability and efficiency.

Withdrawal Rate = a + b / CAPE

where

a is a base rate and b scales how much the CAPE level shifts the rate. When CAPE is high (expensive market), you withdraw a lower percentage; when CAPE is low (cheap market), you withdraw a higher one. This is a research-based adaptive strategy designed to respond to market valuations. See Early Retirement Now — Part 18 for the research behind this approach.

Capital Preservation Rule — If your current withdrawal rate has risen more than the Upper Guardrail percentage above your starting rate (e.g. from 4% to above 4.8% with a 20% guardrail), and you have more than 15 years remaining, your withdrawal is cut by the Adjustment percentage (e.g. 10%).

Prosperity Rule — If your current withdrawal rate has fallen more than the Lower Guardrail percentage below your starting rate (e.g. from 4% to below 3.2% with a 20% guardrail, because the portfolio has grown), your withdrawal is raised by the Adjustment percentage, up to but never exceeding the original starting amount.

The rules fire once per year (at each annual boundary), so your spending adjusts gradually rather than month-to-month.

Important note on real-terms simulation: This simulator works entirely in inflation-adjusted (real) terms — all portfolio values and returns already account for inflation. The original Guyton-Klinger system includes a third rule (the "Inflation Rule") which skips the annual cost-of-living raise in bad years; since there is no nominal raise to skip in a real-terms model, this rule is not applicable here and is not implemented. The two guardrail rules above are the core of the strategy.

The typical defaults — 20% upper guardrail, 20% lower guardrail, 10% adjustment — are a widely-cited starting point. See Early Retirement Now — Part 9 for a detailed analysis.

a and the CAPE coefficient b. Only appears when CAPE-Based Withdrawal is selected. The formula is Withdrawal Rate = a + b / CAPE. Defaults are a = 0.02 (2% base rate) and b = 0.5, which gives roughly 3.4% at a CAPE of 36. A dynamic preview below the fields shows the current implied withdrawal rate using today's live CAPE value.

Upper Guardrail (%) — If the current withdrawal rate exceeds the starting rate by more than this percentage, the Capital Preservation Rule cuts spending by the Adjustment amount. Default: 20%. Example: starting at 4%, if the portfolio shrinks enough that you're now withdrawing at 4.8% or more (20% above 4%), the cut fires.

Lower Guardrail (%) — If the current withdrawal rate falls below the starting rate by more than this percentage, the Prosperity Rule raises spending by the Adjustment amount (up to the original amount). Default: 20%. Example: starting at 4%, if the portfolio has grown such that you're now withdrawing at 3.2% or less (20% below 4%), the raise fires.

Adjustment (%) — The percentage by which the annual withdrawal is raised or cut when a guardrail triggers. Default: 10%.

This is useful when you have non-negotiable fixed expenses (mortgage, medical bills, basic living costs). The floor ensures the simulation does not produce unrealistically low spending in bad market scenarios — but it also increases failure risk, because you are committing to a minimum spend even when the portfolio has fallen.

While this field is marked as 'Optional', it is highly recommended that you set a reasonable value here if using a percentage-based withdrawal methodology, as no one can live on arbitrarily small withdrawals.

Regular income or expense items that supplement (or offset) your portfolio withdrawals. Up to 10 cash flows can be entered.

Because all returns in this simulator are real (inflation-adjusted), a COLA-adjusted cash flow retains its full purchasing power across all simulated years. A non-COLA-adjusted cash flow shrinks in real terms over time.

Common examples: Social Security (positive, perpetual, COLA); a defined-benefit pension (positive, perpetual or to your death, may or may not be COLA); a mortgage that ends in a few years (negative, not perpetual, not COLA); a rental property income (positive, perpetual, not COLA); planned large expenses like college tuition (negative, 4-year window, not COLA).

This section allows you to model a dynamic asset allocation strategy — one that changes your mix of stocks, bonds, and cash over time, rather than holding a fixed allocation. This is entirely optional; most users can skip it and use the allocation set in §2.

A bond tent is a common strategy where you temporarily shift to a more conservative (bond-heavy) allocation around the retirement date to reduce sequence-of-returns risk — the danger that a bad market right at the start of retirement will permanently damage your portfolio. After a few years into retirement, you gradually shift back to a more equity-heavy allocation.

The shape is like a tent: start with moderate equities, increase bond allocation leading into retirement (the rise), hold the conservative peak at retirement, then glide back toward equities (the fall).

The One More Year analysis runs a parallel simulation in which you work for exactly one additional year before retiring, then compares the results to your base scenario. It answers the common pre-retirement question: "If I worked just one more year, how much would it improve my retirement prospects?"

This adds very little to simulation time and produces its own full results section (§3.3 in the results page).

The results page presents a summary scorecard followed by five detailed sections. Below is an explanation of every tile, chart, and number.

The scorecard at the top of the results page gives you the headline numbers at a glance.

Detailed breakdown of the success rate from multiple angles.

How your portfolio evolves over the course of retirement.

How spending plays out in practice across all simulated scenarios.

Two figures are shown: the median worst-5-year average (typical outcome) and the 10th percentile (unlucky-but-plausible — only 1 in 10 paths do worse). This metric captures sequence-of-returns risk more concretely than average withdrawal figures, since it highlights the trough rather than the mean.

If you are using a delayed retirement option (specific date or target portfolio value), lines start from your retirement date, not from today — the pre-retirement period is left blank so the chart does not misleadingly show withdrawals before retirement begins.

The commonly cited "4% rule" refers to an initial withdrawal of 4% of portfolio — but what matters over time is the current withdrawal rate. A withdrawal rate above 8% is generally considered dangerous, particularly in early retirement: it means the portfolio would need consistent high returns just to keep pace with spending, leaving little margin for bad markets.

Filters the full simulation to only the historical starting years where stock market valuations (CAPE ratio) were similar to today's, then shows success rates and portfolio outcomes for that subset.

Rather than summarising all scenarios statistically, this section shows two specific historical paths in detail — what portfolio value and spending would have looked like year-by-year if you had retired at those particular moments in history. Historical stress periods (the Great Depression, stagflation era, dot-com crash, etc.) are annotated on each chart.

Retirement failure is disproportionately a problem for people who live a very long time. This section filters to the top 10% of mortality outcomes (the longest-lived scenarios) and reports what success looks like for that cohort specifically.

The Safe Withdrawal Rate (SWR) section answers: "What fixed annual withdrawal would give me a 100% success rate in this analysis?" It is a closed-form calculation based on depleting the portfolio to zero at the 90th percentile of life expectancy.

The green curve (left axis) shows the fraction of historical paths that survive to your horizon age at that scale factor. The blue band (right axis) shows the median final portfolio at that age, with the interquartile range shaded; paths that go bankrupt contribute $0 to this median. A dashed marker at 100% shows your current plan.

Moving the slider left (spending less) raises the success rate and grows the median final portfolio. Moving it right shows how quickly outcomes deteriorate if you spend more. This helps you calibrate how much margin — or how much headroom — your current withdrawal level leaves.

A note of caution: this scaling does not respect the minimum withdrawal floor you might have set, so could lead to withdrawals that are too small to live on. Please use this chart to gain some insight on how much more or less you have available to spend, but do rerun the analysis with updated withdrawal numbers to see a full simulation of what would happen if you say increase withdrawals by 10%.

Only shown when the One More Year analysis is enabled in the inputs. Compares your base retirement scenario side-by-side with the one-year-delayed scenario.

If this fraction is very high (most growth came from work), it suggests the extra year was particularly valuable because your savings rate is high relative to your portfolio. If low (most came from market returns), working extra was less critical — the portfolio would have grown nearly as much regardless.

Expected capital gains are estimated using long-run historical averages; actual results in any given year could differ significantly.

The simulation uses historical US market data. The future could be worse — or better — than anything in the historical record. Structural economic changes, persistent low growth, deflation, sovereign debt crises, or other scenarios not well-represented in 150 years of US data could produce outcomes outside the historical range.

The historical record is also US-centric. An investor in a single country faces country-specific risk that a global portfolio would diversify away. Past US market performance has been among the strongest in the world — future performance may revert toward global averages.

The reverse mortgage model is intentionally simple: it draws 40% of the home value as a one-time lump sum when the portfolio first reaches zero. Real reverse mortgages involve fees, interest, ongoing qualification requirements, and complex terms. Do not rely on this simplification for detailed home-equity planning; it is only meant to give an idea of how your home equity could help keep your retirement going.

As noted in the results reference, the Safe Withdrawal Rate section does not account for mortality or the reverse mortgage. It will generally report a lower success rate than the main success rate in §2.1, as no reverse mortgage will come to the rescue, and most people do not live to the 90th-percentile age, which is consider the end for our SWR analysis. These are measuring different things and should not be directly compared.

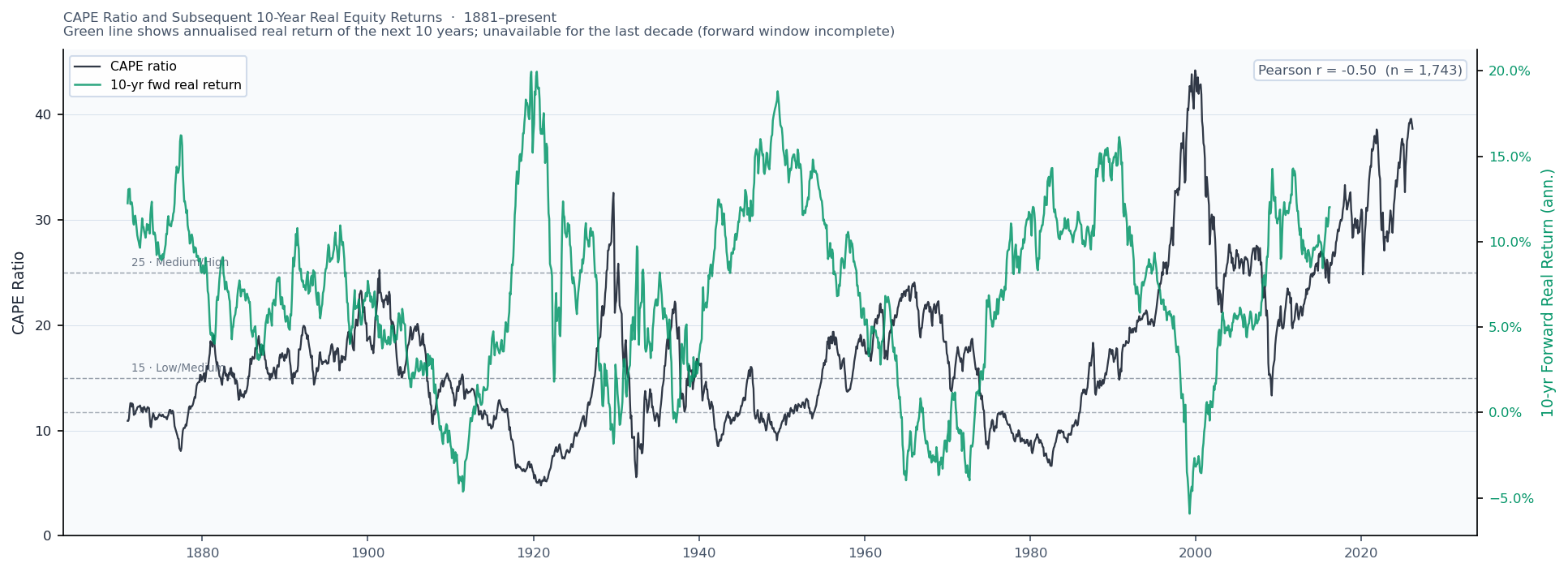

The chart below plots the CAPE ratio since 1881 alongside the annualised real equity return over the following 10 years. The relationship is striking: every major CAPE peak has been followed by a period of weak or negative real returns.

The three previous episodes where CAPE spiked above 25 each preceded a difficult decade for equity investors: the Great Depression (post-1929), the stagflation of the 1970s (post-1966), and the "lost decade" of 2000–2010 (post-dot-com peak). Retirements starting in those windows appear as the hardest scenarios in the simulator. What that implies for the current retiree ... is uncertain, but admittedly disconcerting.

The CAPE-adjusted success rate filters historical scenarios to those with similar stock valuations to today, using three buckets: Low (CAPE ≤ 15, ~45% of history), Medium (15–25, ~42%), and High (>25, ~13%). Because the High bucket covers relatively few historical episodes, the CAPE-adjusted estimate is noisier than the overall rate. Treat it as a directional signal, not a precise number.

The simulation does not model income taxes, capital gains taxes, required minimum distributions, or estate taxes. In practice, these can meaningfully affect the amount available for spending. The withdrawal amount you choose should include any taxes that are due.

The simulation does not model healthcare costs, long-term care needs, inflation in specific expense categories (medical inflation often exceeds general inflation), changes in spending in response to health or lifestyle, or the risk of cognitive decline affecting financial decision-making. These are all real retirement risks that a comprehensive plan must address.